Real StoryHyderabadProduct ManagementAge 43

Had ₹8L at 38. Made three changes. Have ₹1.4Cr at 43.

Submitted via form · April 2026 · Numbers and story are as shared; name and employer removed

Age when started

38

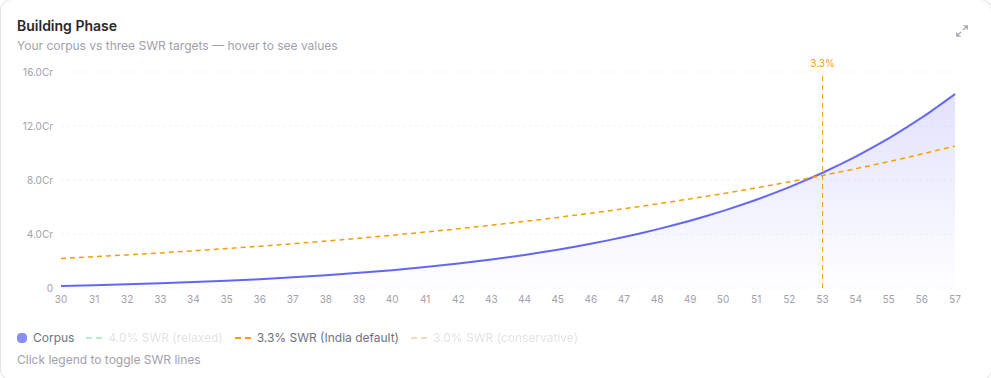

Corpus at 38

₹8L

Corpus today (43)

₹1.4Cr

Monthly investment

₹1.1L

Savings rate

~52%

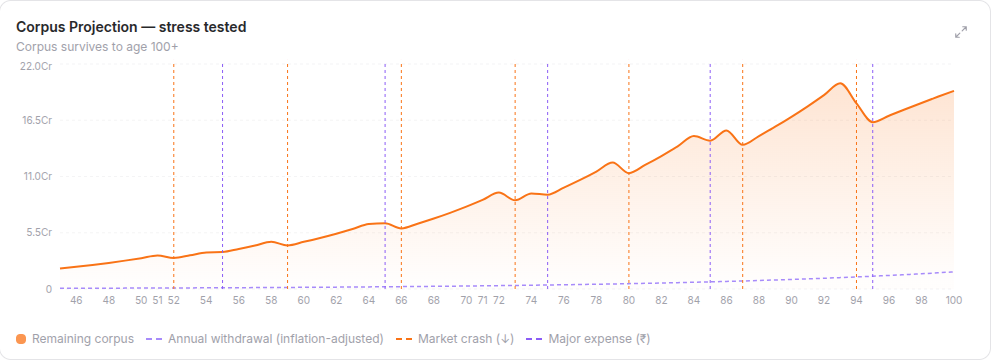

FIRE target

Age 52

What moved the needle

Three things, all in about 18 months. First — moved from Gurgaon to Hyderabad when my company went fully remote. Same salary, same job, rent dropped from ₹38k to ₹18k, eating out got 30-40% cheaper. My FIRE number dropped AND savings rate went up at the same time. One decision, two effects.

Second — moved my parents to Hyderabad instead of sending money home. Was remitting ₹22k/month. Now I send ₹10k and we share some household costs. Also stopped worrying about them every other day, which is harder to put a number on.

Third — closed all FDs, surrendered one old LIC policy (took a haircut on the surrender value, was painful), and moved everything into a Nifty 50 index fund. Started a ₹90k/month SIP. This was the scariest move. It was also the most important.

What set me back

FDs and LIC from 30 to 38. I was earning decent money and felt responsible because I was “saving.” At 38 I had ₹8L. That's eight years of reasonable income with almost nothing to show for it in real terms. FD at 6.5%, taxed at 30% = 4.5% post-tax. Inflation at 5.5–6%. I was going backwards and didn't know it.

The LIC surrender was the worst. Paid premiums for 6 years, surrendered for less than I put in. The agent who sold it to my dad presented it as both insurance and investment. It's neither, not really.

What I'd tell my 28-year-old self

Geography is a financial decision. Where you live changes your FIRE number more than most investment choices — it hits expenses AND corpus target at the same time. Most people treat where they live as fixed. It's not.

And: a “safe” investment that doesn't beat inflation isn't safe. It's just a slower way to lose.