Real StoryBengaluruSoftwareAge 34

Salary tripled in 6 years. Lifestyle didn't. Targeting FIRE at 45.

Submitted via form · April 2026 · Numbers and story are as shared; name and employer removed

Monthly expenses

₹55,000

Monthly investment

₹70,000

Savings rate

~55%

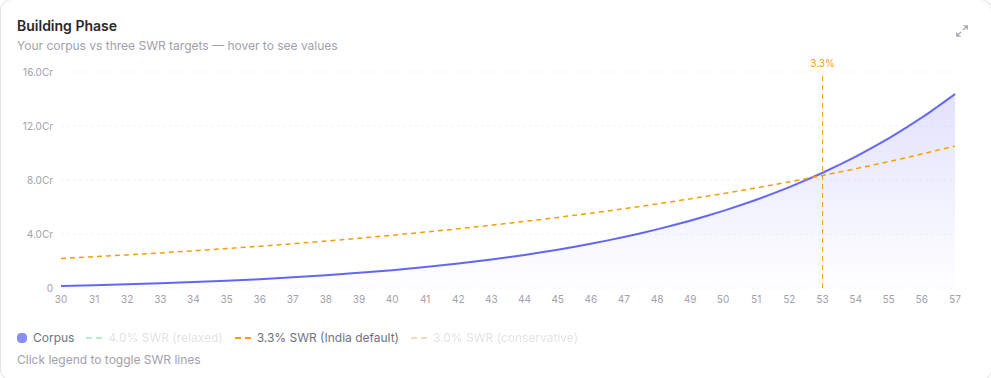

Current corpus

₹62L

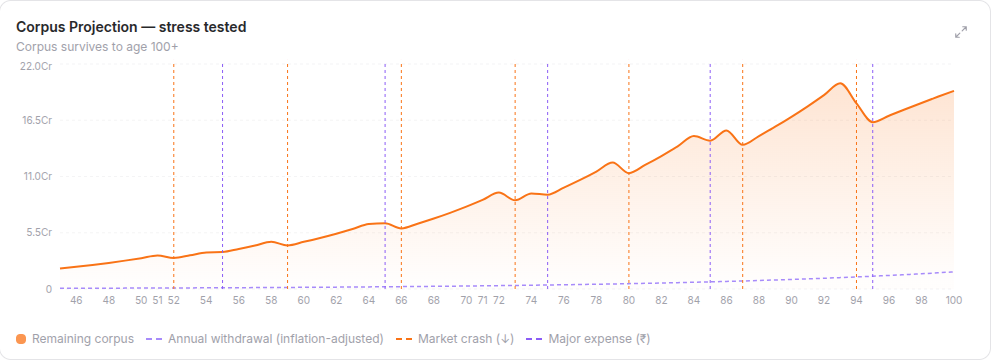

FIRE number (3.3% SWR)

~₹2.1 Cr

FIRE target

Age 45

What moved the needle

Never upgraded lifestyle when salary went up. When I moved from my first job to a product company, CTC jumped from ₹5.8L to ₹14L. I just... didn't change anything. Same flat, same routine. Invested the entire difference. Did the same when it went to ₹22L. Same SIP going up, same flat, one less holiday a year than colleagues. People thought it was weird. My SIP hit ₹70k/month before I turned 33.

What set me back

Maxed VPF for four years because someone told me it was “better than ELSS, tax-free.” It is — if you're retiring at 60. I want to retire at 45. VPF locks until 58. I have ₹5L sitting in a box I can't open for 23 more years. It'll compound fine but I can't SWP from it. For a FIRE plan it's dead weight. Stopped in 2020, everything goes into index funds now.

What I'd tell my 28-year-old self

Understand what “liquid” means before you put money somewhere. Tax-free doesn't matter if you can't access it when you need it. And: the gap between what you earn and what you spend is the only number that actually matters. Keep it wide.